Why “We’ll Just Try a Higher Price First” Usually Backfires

It’s a common thought:

“Let’s start higher and see what happens.”

It sounds harmless — flexible, low risk.

But in stable markets like Bucks County, Montgomery County, and the Main Line, that approach often creates quiet problems.

When a home launches, buyers immediately compare it to recent sales and active competition. If the price feels disconnected from value, most buyers don’t negotiate.

They move on.

The first 7–14 days on market are the strongest visibility window. If pricing misses the mark during that period, momentum can be difficult to rebuild.

Starting high often leads to:

• Fewer early showings

• Longer time on market

• Incremental price reductions

• Weaker negotiating leverage

Strategic pricing isn’t about being conservative.

It’s about protecting value from day one.

If you’re preparing to sell and debating pricing strategy, alignment at launch matters more than testing the ceiling.

It’s one of the most common starting points in listing conversations.

“We’ll just try a higher number and see what happens.”

It sounds harmless.

Flexible.

Low risk.

But in most stable markets — especially in Bucks County, Montgomery County, and along the Main Line or Chestnut Hill areas — that strategy quietly creates problems.

The Market Doesn’t “Try” — It Judges

When a home launches, buyers immediately compare it to:

recent sales

active competition

price-per-square-foot trends

condition and updates

If the price feels disconnected from value, buyers don’t negotiate aggressively.

They move on.

Silently.

There is no trial period.

There is only perception.

The First Impression Window Is Short

The strongest activity typically happens in the first 7–14 days.

That’s when:

Saved searches trigger

Buyers schedule quickly

Agents take notice

If pricing is aligned, that window creates momentum.

If pricing overshoots, that window passes without full engagement.

And once it passes, regaining urgency becomes harder.

Buyers Watch Patterns

Today’s buyers monitor:

Days on market

Price changes

Relisting history

When they see a home start high and reduce later, it shifts perception.

Instead of asking, “Is this worth it?”

They begin asking, “What’s wrong with it?”

That’s not emotion.

That’s psychology.

Strategic Pricing Isn’t Conservative — It’s Controlled

Pricing correctly from the start doesn’t mean underpricing.

It means aligning with:

current buyer demand

competitive inventory

absorption rate

real-time feedback

A disciplined launch creates:

stronger early traffic

better negotiating leverage

clearer buyer perception

It protects value.

The Bottom Line

Testing a higher price feels safe.

But in many cases, it quietly costs time and leverage.

Momentum is strongest at launch.

Precision at the beginning often produces better outcomes than adjustment later.

The goal isn’t to “see what happens.”

It’s to position intentionally from day one.

Get your free real home value at WhatsMyHouseWorthPA.com

The Difference Between Selling a $600K Home and a $1.6M Home in PA

Not all homes sell the same way — and price point changes more than just the number.

In Bucks County, Montgomery County, and along the Main Line, a $600K home and a $1.6M home operate in very different buyer environments.

At $600K:

• Larger buyer pool

• Faster timelines

• Strong competition

At $1.6M:

• Narrower, more deliberate buyer pool

• Longer decision cycles

• Greater pricing precision required

• Elevated presentation expectations

Higher price points demand a different rhythm — in marketing, positioning, and negotiation.

Success isn’t about treating every listing the same.

It’s about aligning strategy with the segment.

If you’re preparing to sell and wondering how your price tier changes the approach, I recently broke this down in more detail.

Not all homes sell the same way.

And price point changes more than just the number.

In Bucks County, Montgomery County, and along the Main Line and Chestnut Hill areas, a $600,000 home and a $1.6M home operate in very different environments — even within the same town.

Understanding that difference matters.

The Buyer Pool Is Different

At $600K:

The buyer pool is larger

Financing is common

Competition can be strong

Timelines tend to move faster

At $1.6M:

The buyer pool narrows

Cash or strong financial backing is more common

Decision cycles are longer

Negotiations are more deliberate

It’s not about better or worse.

It’s about scale.

Exposure Strategy Changes

Mid-range homes often benefit from:

Broad exposure

Strong opening-weekend activity

Competitive pricing that invites momentum

Higher-priced homes require:

Elevated presentation

Precision targeting

Controlled showing schedules

Patience in marketing cycles

The strategy shifts with the audience.

Pricing Sensitivity Increases at the Top

In mid-range segments, a slight pricing miss can still generate traffic.

In higher brackets, pricing precision becomes critical.

Overpricing in luxury segments can:

Quietly stall momentum

Extend timelines

Shift negotiating leverage

Buyers at this level are informed and analytical.

They don’t rush.

Presentation Expectations Rise

Photography, staging, and condition matter at every price point.

But at $1.6M and above, expectations increase significantly.

Buyers expect:

Cohesive design

Strong lighting and imagery

Detailed marketing materials

Clear positioning within the neighborhood

The marketing must match the value.

Negotiation Style Evolves

Mid-range negotiations often focus on:

Inspection items

Appraisal gaps

Financing contingencies

Higher-end negotiations may center on:

Terms

Timing

Personal property

Privacy

Structure of the deal

It becomes less transactional and more strategic.

The Bigger Picture

Selling a $600K home well requires skill.

Selling a $1.6M home well requires a different rhythm.

Both require discipline.

But the approach cannot be identical.

Understanding the psychology of each price tier protects leverage.

The Bottom Line

Price point changes:

buyer behavior

marketing strategy

timeline expectations

negotiation dynamics

Success isn’t about treating every listing the same.

It’s about aligning strategy with the segment.

Visit SellMyHouseinPA.com to get a free plan based on your timeline

How Buyers Actually Search for Homes in 2026

The way buyers search for homes has evolved — but not in the way most people think.

Yes, buyers start online. They use saved searches, apps, alerts, and multiple platforms.

But serious buyers don’t rely on just one source.

Today’s buyers:

• Track new listings instantly through alerts

• Compare homes across multiple platforms

• Watch price changes and days on market

• Research neighborhoods before scheduling showings

• Rely on agent guidance to validate value

The first days on market matter more than ever because visibility across platforms drives early momentum.

Exposure, pricing alignment, and presentation now influence not just buyers — but algorithms.

Understanding how buyers search directly impacts how a home should be launched.

If you’re preparing to sell, strategy begins before the listing goes live.

The way buyers search for homes has changed.

But not in the way most people think.

It’s not just about new apps or flashy platforms. It’s about behavior.

And buyer behavior today is layered.

1. Buyers Start Online — But They Don’t Stop There

Most buyers begin their search digitally.

They:

Browse listing portals

Set up saved searches

Track price changes

Compare properties over time

But serious buyers don’t rely on one source.

They cross-reference:

public portals

agent alerts

private networks

off-market conversations

Visibility across multiple channels matters more than ever.

2. Alerts Create Immediate Awareness

The first exposure window is powerful.

When a home hits the market:

Saved search alerts trigger instantly

Buyers receive push notifications

Agents notify active clients

That early surge often determines how a listing performs.

Miss that window, and momentum can soften.

3. AI and Algorithm Sorting Is Real

Today’s platforms use algorithmic sorting to prioritize listings.

Properties are shown based on:

engagement levels

pricing alignment

freshness

buyer search behavior

That means pricing and presentation influence not just buyers — but platform visibility.

4. Buyers Research Quietly

Many buyers watch for weeks before ever scheduling a showing.

They:

Monitor days on market

Track price adjustments

Compare condition

Study neighborhood sales

By the time they step inside a property, they often already have strong opinions.

The listing experience must match expectations.

5. Agent Relationships Still Matter

Despite all the technology, serious buyers still rely heavily on agents.

They ask:

Is this priced correctly?

How competitive will this be?

Is there room to negotiate?

Are there properties coming soon?

Digital discovery starts the process.

Professional guidance shapes the decision.

What This Means for Sellers

Because buyers search in layers, sellers benefit from:

strong pricing alignment

professional photography

coordinated launch timing

broad exposure

agent-to-agent communication

A home isn’t competing only with what buyers see on one app.

It’s competing across platforms, alerts, networks, and perception.

The Bottom Line

Buyers today are:

informed

alert-driven

comparison-focused

influenced by both technology and relationships

Understanding how they search directly impacts how a home should be launched.

Exposure is no longer optional.

It’s strategic.

Wondering HowDoISellMyHouseInPA visit this site

The Hidden Risk of Overpricing in a Stable Market

In a fast-rising market, overpricing can sometimes be hidden.

In a stable market, it can’t.

Today’s buyers in Bucks County, Montgomery County, and the Main Line are informed. They see comparable sales, price trends, and competition instantly.

When a home launches above where the market sees value, buyers often don’t negotiate.

They move on.

The first days on market matter most. That early window creates momentum. If pricing misses the mark, regaining that momentum becomes harder.

Overpricing doesn’t always cause dramatic failure.

More often, it causes:

• Fewer showings

• Extended timelines

• Incremental reductions

• Weakened negotiating leverage

Pricing isn’t about testing the highest number.

It’s about aligning with the market from the start.

In stable conditions, precision protects value.

In a rapidly rising market, overpricing can sometimes be masked.

In a stable market, it cannot.

That difference matters.

In Bucks County, Montgomery County, and along the Main Line, and Chestnut Hill areas, many segments have moved from aggressive appreciation into steadier conditions. Homes are still selling — but buyers are more measured.

And that changes how pricing works.

Why Overpricing Feels Safer Than It Is

Some sellers believe pricing high “leaves room to negotiate.”

The logic sounds reasonable:

Start strong

See what happens

Adjust later if needed

But today’s buyers are informed.

They see:

recent comparable sales

price-per-square-foot trends

inventory levels

previous listing history

If a property feels disconnected from value, many buyers simply move on.

Silently.

The First Impression Window Is Short

When a home hits the market, it enters a high-visibility phase.

Saved searches trigger.

Buyers schedule quickly.

Agents take notice.

This early window is when momentum is strongest.

If pricing misses the mark, the listing can:

receive fewer showings

generate cautious feedback

lose competitive positioning

And once momentum slows, regaining it becomes harder.

The Compounding Effect of Time

In stable markets, time carries more weight.

As days on market increase:

buyers begin to question value

negotiating leverage shifts

competing properties gain advantage

An initial overpricing strategy can quietly erode negotiating power.

Not dramatically — but steadily.

Precision Matters More Than Optimism

Pricing isn’t about testing the highest possible number.

It’s about aligning with:

current buyer psychology

comparable activity

absorption rate

competition at that price tier

In many cases, strategic precision creates stronger outcomes than ambitious starting points.

Especially in steady markets.

The Bigger Picture

Overpricing doesn’t always result in dramatic failure.

More often, it results in:

extended timelines

incremental reductions

negotiation from a weakened position

The risk isn’t that a home won’t sell.

The risk is that it sells from disadvantage.

The Bottom Line

In a stable market, pricing discipline protects value.

Momentum is strongest at launch.

Precision creates leverage.

Optimism without alignment creates friction.

The goal isn’t to price high.

It’s to price correctly.

To get an accurate home value check out: WhatsMyHouseWorthPA.com where I provide you with a free report that gives you an accurate number based on the market. The absolute Gold Standard in home valuation. FREE.

Why Main Line Homes Attract a Different Type of Buyer

Not all buyers think the same — and Main Line buyers are no exception.

In areas like Bryn Mawr, Wayne, Villanova, and Haverford, purchasing decisions tend to be more deliberate.

These buyers are often:

• Highly researched

• Long-term focused

• Sensitive to presentation and pricing

• Evaluating lifestyle, not just square footage

School districts, architectural character, location, and long-term value all carry weight.

That also means timelines can look different. A slightly longer marketing period isn’t necessarily a red flag — it’s often part of a more thoughtful decision cycle.

Selling in these areas requires nuance, positioning, and patience.

Understanding the buyer matters just as much as pricing the home.

Not all markets behave the same.

And not all buyers think the same.

Homes along the Main Line — including areas like Bryn Mawr, Wayne, Villanova, Devon, and surrounding communities — tend to attract a different type of buyer than other parts of the region.

Understanding that difference matters.

It’s Not Just About Price

Yes, many Main Line homes carry higher price tags.

But the distinction isn’t just financial.

It’s behavioral.

Buyers in these areas are often:

Highly researched

Patient

Education-focused

Long-term oriented

Sensitive to presentation and positioning

They are not typically impulse-driven.

They compare carefully.

Lifestyle Over Square Footage

In many Main Line neighborhoods, buyers are purchasing more than a house.

They’re buying:

School district reputation

Architectural character

Community history

Proximity to institutions and transit

Long-term stability

That shifts how decisions are made.

A home isn’t simply evaluated by size and price.

It’s evaluated in context.

Presentation Carries More Weight

Because buyers are deliberate, presentation matters.

Photography, staging, and narrative positioning play a stronger role.

Minor details that might be overlooked elsewhere often become meaningful here.

Condition and pricing alignment are scrutinized more closely.

Longer Decision Cycles Are Normal

In higher price brackets and established neighborhoods, timelines can stretch.

Buyers may:

View multiple properties more than once

Consult advisors or family

Analyze value relative to historical sales

Negotiate thoughtfully

A slightly longer days-on-market number does not automatically signal weakness.

In these areas, patience is often part of the process.

Seller Expectations Must Align

One of the biggest disconnects happens when sellers expect Main Line homes to behave like faster-moving mid-range markets.

They don’t.

Success often comes from:

Strategic pricing

Proper launch timing

Elevated presentation

Controlled negotiation

Not urgency.

The Bigger Picture

The Main Line is not just a geographic label.

It’s a buyer psychology environment.

Understanding how those buyers think — and how they evaluate value — directly influences how a home should be positioned.

Selling in these areas requires nuance.

Not volume.

The Bottom Line

Main Line homes attract buyers who are:

deliberate

informed

long-term focused

That’s not a challenge.

It’s simply a different rhythm.

When the strategy matches the buyer, the process becomes far more predictable.

To explore what its like to LiveOnTheMainLine click here

What Happens Before a Home Hits the Market

Most buyers only see the moment a home goes live.

What they don’t see is everything that happens beforehand.

Strong results usually come from preparation — not luck.

Before a property ever hits the MLS, smart sellers focus on:

• Pricing strategy

• Competitive positioning

• Minor repairs & presentation

• Professional photography

• Exposure planning

The first days on market matter most. A rushed launch can create hesitation. A prepared launch creates momentum.

In Bucks County, Montgomery County, and the Main Line, the homes that perform best are rarely accidental — they’re intentional from the start.

If you’re thinking about selling, preparation begins well before the listing date.

Most buyers only see the moment a property goes live.

Photos.

Price.

Description.

Availability.

But what determines how a home performs often happens before it ever appears online.

In Bucks County, Montgomery County, and the Main Line, preparation frequently makes the difference between momentum and stagnation.

1. Strategy Comes First — Not the Sign

Before photography, showings, or MLS exposure, the first step is clarity.

That includes:

Seller priorities (price, timing, privacy, convenience)

Current market positioning

Competitive inventory

Price band sensitivity

A home isn’t simply “listed.”

It’s positioned.

And positioning begins well before the public sees anything.

2. Pricing Is Built, Not Guessed

Strong pricing isn’t about picking a number that feels good.

It requires:

Reviewing recent comparable sales

Analyzing active competition

Evaluating price-per-square-foot trends

Understanding buyer psychology in that segment

In some cases, slightly underpricing invites competition.

In others, precision is critical.

Pricing decisions made early shape everything that follows.

3. Presentation Planning

Buyers don’t compare homes in isolation.

They compare:

condition

lighting

staging

photography quality

layout flow

emotional appeal

Before launch, preparation may include:

minor repairs

cosmetic adjustments

decluttering

strategic staging

scheduling professional photography

These aren’t cosmetic details.

They influence perceived value.

4. Exposure Strategy

Not every home should launch the same way.

Some require:

full-scale public exposure

coordinated showing windows

strong opening weekend activity

Others may benefit from:

pre-market conversations

targeted buyer outreach

phased marketing

The right exposure plan depends on property type and seller goals.

5. Timing Matters

Even in stable markets, timing influences perception.

Launching:

into heavy competition

at the wrong price tier

or without full preparation

can create unnecessary friction.

A well-timed launch creates clarity and urgency.

A rushed one creates doubt.

The Bigger Picture

Buyers see listings.

Sellers should focus on preparation.

What happens before a home hits the market often determines:

the strength of early activity

buyer perception

negotiating leverage

and ultimately, final outcome

Good marketing begins before marketing.

The Bottom Line

A listing is not a starting point.

It’s the result of decisions made beforehand.

In Bucks County, Montgomery County, and the Main Line, the homes that perform best are rarely accidental.

They’re intentional from the start.

If you’re looking for a plan based on your timeline check out SellMyHouseinPA.com to get a free roadmap of your listing journey.

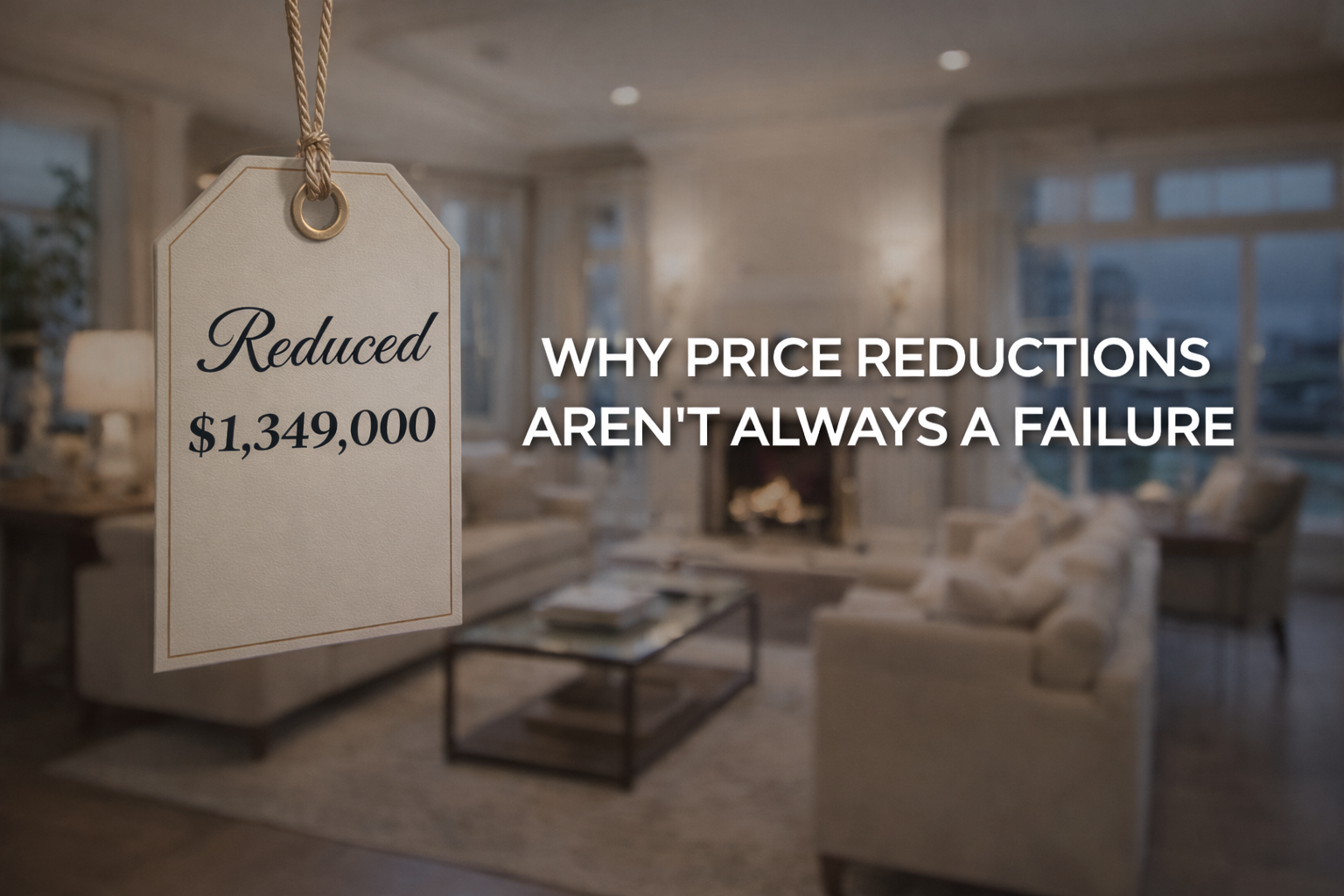

Why Price Reductions Aren’t Always a Failure

The words “price reduction” make many sellers nervous.

But in many cases, an adjustment isn’t failure — it’s strategy.

When a home first hits the market, pricing sends a signal. Within the first few weeks, buyer activity and feedback provide real-world data.

If interest is lighter than expected, it doesn’t mean something is wrong. It may simply mean the market is giving feedback.

A timely adjustment can:

• Re-engage serious buyers

• Restore positioning

• Prevent long-term stagnation

• Protect overall value

Holding firm at the wrong number often costs more than making a smart, early move.

Pricing isn’t about ego. It’s about alignment.

If you’re watching your home sit and wondering what it really means, I recently broke this down in more detail.

Few words create more anxiety for a seller than “price reduction.”

It feels like something went wrong.

It feels like the market rejected the home.

It feels personal.

But in many cases, a price adjustment isn’t a failure.

It’s strategy.

What a Price Really Represents

When a home first hits the market, the price is a signal.

It communicates:

positioning

expectations

target buyer pool

perceived value

But the market is not theoretical.

It responds in real time.

Showings, buyer feedback, and comparable activity begin shaping a clearer picture within the first few weeks.

That feedback isn’t emotional. It’s data.

The First 14–21 Days Matter Most

In Bucks County, Montgomery County, and the Main Line, the strongest activity typically happens early.

When a home launches:

buyers who’ve been waiting see it immediately

saved searches trigger alerts

serious buyers schedule quickly

If interest is lighter than expected, it doesn’t automatically mean the home is undesirable.

It may mean the pricing and buyer perception aren’t fully aligned.

That’s not failure. That’s feedback.

Why Holding Firm Isn’t Always Strong

Some sellers believe holding the original price at all costs signals confidence.

In reality, prolonged stagnation can create the opposite effect.

As days on market increase:

buyers begin to wonder what they’re missing

competing properties gain momentum

leverage shifts quietly

A timely adjustment can reset attention and restore positioning.

It’s not retreating.

It’s recalibrating.

Not All Reductions Are Equal

There’s a difference between:

Reactive reductions made out of panic

Strategic adjustments based on real market signals

The first creates instability.

The second demonstrates responsiveness and control.

When done correctly, a pricing shift can:

re-engage serious buyers

spark renewed activity

prevent long-term erosion

Context Always Matters

A price adjustment means something very different depending on:

the town

the price point

overall inventory levels

buyer demand in that segment

In higher price brackets, longer timelines and adjustments are normal.

In competitive mid-range markets, precision matters more quickly.

There is no universal rule.

Only context.

The Bigger Picture

The goal of pricing isn’t to “win” against the market.

It’s to position the home in a way that:

attracts the right buyers

protects value

creates competition when possible

avoids long-term stagnation

Sometimes that requires adjustment.

And adjustment, when done intentionally, is not weakness.

It’s discipline.

The Bottom Line

A price reduction isn’t automatically a red flag.

It’s a response to information.

In many cases, it’s the move that protects a seller from larger losses later.

What matters isn’t whether the price changes.

What matters is whether the strategy remains intentional.

If you’re concerned about pricing your home correctly visit WhatsMyHouseWorthPA.com to get your real home value prepared personally by Josh Wernick Pricing Strategy Advisor and Luxury Homes Certified Agent.

What “Days on Market” Actually Means in Bucks and Montgomery County

“Days on Market” is one of the most misunderstood numbers in real estate.

It simply measures how long a home has been listed before going under contract. It does not measure quality, value, or desirability.

In Bucks County, Montgomery County, and the Main Line, DOM varies significantly based on:

• Town

• Price range

• Buyer pool

• Property type

A $650K home and a $1.6M home in the same area behave very differently.

Time on market only becomes meaningful when paired with context — showings, feedback, and comparable activity.

If you’re watching the market and wondering what the numbers actually mean for your home, I recently broke it down in more detail.

What “Days on Market” Actually Means in Bucks and Montgomery County

Sellers watch it closely.

Buyers reference it constantly.

Agents talk about it as if it’s a verdict.

But “Days on Market” — often shortened to DOM — is one of the most misunderstood numbers in real estate.

Especially in Bucks County, Montgomery County, and the Main Line.

What Days on Market Really Measures

Days on Market simply tracks how long a property has been actively listed before going under contract.

That’s it.

It does not measure:

quality

desirability

seller motivation

long-term value

It measures time.

And time only becomes meaningful when paired with context.

Why DOM Varies So Much by Town

A 14-day listing in one town can feel slow.

A 30-day listing in another can be completely normal.

For example:

In certain price ranges in Newtown or Doylestown, strong demand can compress timelines.

In parts of the Main Line, higher price points often mean longer, more deliberate buyer decision cycles.

In niche or luxury segments, extended marketing periods are common and expected.

DOM is not universal. It is hyperlocal.

That’s why comparing one town to another rarely tells the full story.

Why Price Point Matters More Than Town Alone

Even within the same neighborhood, DOM can change dramatically depending on price.

Entry-level homes tend to move faster.

Mid-range homes respond heavily to pricing precision.

High-end homes often require patience and targeted exposure.

A $650,000 home and a $1.6M home in the same zip code do not behave the same way.

Looking at DOM without separating by price tier leads to false conclusions.

When DOM Becomes a Signal

Days on Market only becomes meaningful when:

Showings slow significantly

Buyer feedback repeats consistently

Comparable homes are selling faster

Pricing and presentation are misaligned

At that point, DOM becomes feedback — not failure.

Why Sellers Shouldn’t Panic Over the Number

Sellers sometimes interpret 21 days, 30 days, or 45 days as a red flag.

In reality:

Some homes attract immediate competition.

Others require strategic patience.

Many fall somewhere in between.

A property sitting for a few weeks in a stable market does not automatically signal a problem.

It signals that buyers are evaluating.

The Bigger Picture

Days on Market is one metric among many.

The more important questions are:

Are qualified buyers viewing the property?

Is feedback consistent?

Is the pricing aligned with current buyer expectations?

Is exposure reaching the right audience?

Time without context creates anxiety.

Time with context creates clarity.

The Bottom Line

In Bucks County, Montgomery County, and the Main Line, DOM varies by:

town

price range

buyer pool

property type

It’s not a universal scoreboard.

It’s a data point.

And like all data points, it only matters when interpreted correctly.

Whats your house actually worth? Visit: WhatsMyHouseWorthPA.com for a free in depth report

Why Some Homes Sell Quietly — And Why Most Shouldn’t

Some homeowners consider selling quietly — without a sign, without broad exposure, and without public marketing.

In certain situations, that approach makes sense. Privacy, flexibility, or testing the waters can all be valid reasons.

But for most homes in Bucks County, Montgomery County, and the Main Line, broad exposure creates competition — and competition protects value.

I recently wrote about when off-market strategies work, and when full market visibility is the stronger move.

Every seller eventually hears about it.

A neighbor sells without a sign in the yard.

A friend says their home “never even hit the market.”

Someone mentions a private buyer was found quickly and discreetly.

It sounds efficient. Clean. Simple.

But the truth is more nuanced than that.

What “Off-Market” Actually Means

An off-market sale simply means the property was not broadly marketed through the MLS and public listing platforms.

Instead, it may have been:

shared privately with a limited group of buyers

offered through agent networks

presented quietly to pre-qualified prospects

tested before a full public launch

There’s nothing inherently wrong with that.

In certain situations, it can make sense.

When Selling Quietly Can Be Smart

There are real scenarios where discretion matters:

A seller values privacy over maximum exposure

The property is highly unique and needs controlled positioning

The seller wants to test pricing before committing publicly

Timing is uncertain, and flexibility matters

In these cases, a quiet approach can reduce stress and give the seller space to make decisions.

But that’s not the same thing as maximizing outcome.

What Quiet Selling Trades Away

When a home is not publicly exposed, it gives up something important:

competition.

The open market creates:

urgency

comparison

multiple-offer scenarios

broader buyer awareness

Without exposure, you’re relying on:

whoever happens to already be looking

whoever is connected to the right agent

whoever hears about it informally

That can work — but it narrows the field.

And when the field narrows, leverage often narrows with it.

Why Most Homes Still Benefit From Public Exposure

For the majority of properties, especially in Bucks County, Montgomery County, and the Main Line, broad exposure creates stronger results.

Public listings:

generate more buyer activity

increase perceived demand

encourage faster decision-making

protect sellers from underpricing

Even in stable markets, visibility matters.

In high-equity areas, it matters even more.

The Real Question Sellers Should Ask

Instead of asking:

“Should I sell off-market?”

A better question is:

“What outcome matters most to me?”

If privacy is the priority, a quiet strategy may fit.

If maximizing price and competition matters most, public exposure is usually the stronger path.

A Balanced Approach

Sometimes the right strategy isn’t strictly one or the other.

A seller might:

explore private interest first

assess buyer response

then decide whether to launch publicly

Other times, going directly to the open market is clearly the best move.

The key isn’t chasing what sounds exclusive.

It’s aligning the strategy with the goal.

The Bottom Line

Quiet sales aren’t magic.

They’re simply one option.

Most homes benefit from visibility.

Some benefit from discretion.

The right choice depends on:

the property

the seller’s priorities

and the market context at the time

The important part isn’t whether a home is “off-market.”

It’s whether the strategy is intentional.

If you’re looking for Off-Market Sales or would like to learn about my process for Off-Market Listings, check out: PARealEstateDeals.com

What Actually Matters to Buyers When They Tour Your Home

What Actually Matters to Buyers When They Tour Your Home

Sellers often assume buyers walk into a home evaluating it the same way they do.

They don’t.

Buyers aren’t auditing your decisions or judging your taste.

They’re answering a much simpler internal question:

“Can I see myself living here?”

Understanding what actually influences that decision helps sellers focus on the things that matter — and ignore the noise that doesn’t.

Buyers decide emotionally first, then justify logically

This happens faster than most sellers expect.

Within minutes, buyers form a general impression:

how the home feels

whether it’s comfortable

whether it matches their expectations for the area

whether anything feels off

Details come later.

If the emotional response is positive, buyers work hard to justify the home logically.

If it’s negative, no amount of explanation fixes it.

Light, space, and flow matter more than finishes

Buyers consistently respond to:

natural light

how rooms connect

ceiling height and openness

whether the layout feels intuitive

They notice these things before:

appliance brands

countertop materials

fixture styles

A dated kitchen in a bright, well-laid-out home often outperforms a renovated kitchen in a dark or awkward space.

Cleanliness signals care, not perfection

Buyers don’t expect homes to be flawless.

They do expect them to feel:

clean

maintained

respected

Cleanliness tells buyers:

the home has been looked after

issues haven’t been ignored

ownership has been responsible

That perception carries more weight than cosmetic upgrades.

Buyers compare your home to others immediately

No home is viewed in isolation.

Buyers are constantly comparing:

price relative to nearby homes

size relative to other options

condition relative to expectations for the area

This comparison happens subconsciously.

If something feels out of balance — price, presentation, or expectation — buyers don’t always articulate it.

They just move on.

Over-personalization creates distance

Highly personalized spaces can unintentionally make it harder for buyers to project themselves into the home.

This doesn’t mean stripping personality entirely —

it means reducing friction.

The goal isn’t to impress buyers with taste.

It’s to give them room to imagine their own.

What buyers care about less than sellers think

Buyers are usually less concerned about:

minor cosmetic imperfections

small maintenance items

furniture style

décor choices that can be changed

They are more concerned with:

how the home feels

whether it aligns with their lifestyle

whether it feels appropriately priced for what it offers

That difference is important.

The bottom line

Buyers don’t walk through homes looking for reasons to reject them.

They’re looking for reasons to say yes.

Homes that:

feel welcoming

present clearly

align with expectations

and don’t create friction

…tend to perform better than homes that try to impress on paper alone.

When sellers understand what buyers are actually responding to, decisions become simpler — and results tend to follow more naturally.

What Sellers Can Control (And What They Can’t)

What Sellers can control and what they can’t

One of the biggest sources of stress for sellers isn’t the market itself.

It’s trying to control things that simply aren’t controllable — while overlooking the things that are.

Understanding the difference makes the entire process feel calmer and far more manageable.

What sellers cannot control

Let’s start here, because this is where frustration usually comes from.

Sellers cannot control:

the number of buyers active at any given moment

interest rate headlines

how long a specific buyer takes to decide

emotional reactions from strangers touring the home

broader economic narratives

Trying to manage these things usually leads to second-guessing and anxiety — without improving outcomes.

The market does what it does.

What sellers can control (and this matters more)

What sellers can control has a much bigger impact than most people realize.

1. Pricing clarity

Not just the number — the signal it sends.

Clear pricing tells buyers:

this seller is serious

expectations are realistic

negotiation will be rational

Unclear pricing creates hesitation, not flexibility.

2. Presentation and first impression

Buyers form opinions quickly.

What sellers can control:

cleanliness

light

flow

how the home feels emotionally

First impressions are not superficial.

They’re decisive.

3. Positioning in the market

This is about context, not features.

How your home is positioned relative to:

similar homes

nearby towns

competing listings

…shapes how buyers interpret value.

Positioning is proactive.

Waiting is not.

4. Response to feedback

Feedback isn’t a verdict.

It’s information.

Sellers who respond thoughtfully — instead of defensively — keep leverage longer and make better adjustments when needed.

5. Their own emotional posture

This is the most overlooked factor.

Calm sellers:

negotiate better

make fewer reactive decisions

keep options open

avoid unnecessary standoffs

Emotion doesn’t disappear from selling —

but it doesn’t have to drive decisions either.

Why focusing on control changes outcomes

When sellers focus on what they can’t control, everything feels risky.

When they focus on what they can control, the process becomes clearer:

decisions feel intentional

uncertainty feels manageable

outcomes feel earned, not lucky

That shift alone often improves results.

The bottom line

Selling a home isn’t about predicting the market perfectly.

It’s about:

controlling the variables that matter

letting go of the ones that don’t

making calm decisions with real information

Sellers don’t need total certainty to succeed.

They need clarity about where their influence actually is.

And once that’s clear, the process becomes much easier to navigate.

Selling in Bucks County vs. Montgomery County: What’s Different

Bucks County v. Montco home sales, what’s the difference?

On paper, Bucks County and Montgomery County sit next to each other.

In practice, they behave very differently when it comes to selling a home.

Understanding those differences helps sellers set better expectations — and make cleaner decisions from the start.

Buyer motivation isn’t the same

Bucks County buyers often lead with:

lifestyle

space

character

long-term use

Many are:

upsizing

relocating from denser areas

prioritizing land, charm, or school districts

willing to trade convenience for feel

Montgomery County buyers, on the other hand, are more likely to lead with:

commute

efficiency

proximity

comparison across neighborhoods

That difference alone changes how homes are evaluated.

Comparison behavior looks different

In Montgomery County, buyers tend to compare:

street vs street

neighborhood vs neighborhood

price per square foot more tightly

They’re often evaluating multiple similar options at once.

In Bucks County, comparisons are broader:

town vs town

property type vs property type

lifestyle fit vs pure metrics

That makes Bucks County buyers more selective — but sometimes more decisive once they commit.

Pricing sensitivity shows up in different ways

Montgomery County markets tend to:

respond quickly to price signals

reward precision

penalize overreach early

Small pricing misalignments are noticed quickly because buyers are actively comparing similar homes.

Bucks County pricing is often more elastic:

homes are more unique

comps are less interchangeable

buyers expect variation

That doesn’t mean pricing matters less —

it means justification matters more.

Time on market is interpreted differently

buyers notice days on market

stale listings raise questions

momentum matters early

In Bucks County:

longer consideration periods are more common

buyers expect uniqueness

time alone doesn’t always signal a problem

The same timeline can be read very differently depending on where the home is located.

Presentation expectations vary

Montgomery County buyers tend to respond strongly to:

clean presentation

clarity

move-in readiness

efficiency of layout

Bucks County buyers are often more tolerant of:

older finishes

quirks

character

properties that need vision

But they are less forgiving if a home’s story isn’t clear.

What this means for sellers

The biggest mistake sellers make is assuming:

“A good strategy is a good strategy everywhere.”

It isn’t.

Successful selling depends on:

understanding buyer motivation

knowing how comparison happens

positioning the home accordingly

setting expectations that match the county, not just the price

What works well in one county can quietly underperform in the other.

The bottom line

Bucks County and Montgomery County are close geographically —

but they operate on different buyer psychology.

When sellers understand those differences, decisions feel less confusing and outcomes feel more predictable.

When they don’t, the market tends to correct the misunderstanding on its own.

And it’s rarely subtle when it does.

Why Main Line Homes Behave Differently Than the Rest of Pennsylvania

Why Main Line Homes Behave Differently Than the Rest of Pennsylvania

Not all housing markets behave the same — even within the same county.

Check out livingonthemainline.com

The Main Line is a good example of that.

On the surface, a home is a home.

In practice, Main Line properties follow a different set of buyer expectations, comparisons, and decision patterns than much of the rest of Pennsylvania.

Understanding that difference matters if you’re selling there.

Buyers on the Main Line don’t search like typical buyers

Many Main Line buyers aren’t starting with:

a specific house

a strict price ceiling

a single must-have checklist

They’re starting with:

a location

a school district

a reputation

a lifestyle assumption

That means homes are evaluated less in isolation and more as part of a market narrative.

Your home isn’t just competing against similar properties —

it’s competing against how buyers feel about the area as a whole.

Comparison behavior is more intense

Main Line buyers almost always compare across towns.

It’s common for buyers to look at:

Those comparisons aren’t just about price per square foot.

They’re about:

perceived prestige

commute assumptions

long-term value

social signaling

That comparison pressure changes how homes are priced and positioned.

Price sensitivity works differently

In many markets, buyers hit a hard ceiling and stop.

On the Main Line:

buyers are often more flexible

but more selective

and far more perceptive

They’ll stretch for:

the right street

the right presentation

the right positioning

But they’ll walk quickly if something feels off — even if the home itself is objectively good.

Momentum matters more here than discounts.

Time on market is interpreted differently

In some areas, time on market is ignored.

On the Main Line, buyers notice.

A listing that lingers can quietly raise questions:

Was it overpriced?

Is something wrong?

Is the seller difficult?

That doesn’t mean homes must sell instantly —

but it does mean early positioning carries more weight.

First impressions last longer in comparison-driven markets.

Emotion is present — but expressed differently

Main Line buyers are still emotional buyers.

They just express it through:

deliberation instead of urgency

comparison instead of impulse

justification instead of excitement

This makes the process feel calmer —

but it also makes mistakes harder to reverse once opinions form.

What this means for sellers

Selling on the Main Line isn’t harder —

but it is less forgiving.

Success depends on:

clear positioning from day one

understanding how buyers compare

aligning price, presentation, and perception

recognizing that location context matters as much as the home itself

Generic strategies tend to underperform here.

The bottom line

The Main Line behaves differently because buyers behave differently.

Homes aren’t just evaluated on features —

they’re evaluated on where they sit in the larger conversation about the area.

When sellers understand that, decisions become clearer and outcomes become more predictable.

And when they don’t, the market usually teaches the lesson for them.

Why Pricing Your Home “Just to Test the Market” Usually Creates Problems

Why Pricing Your Home “Just to Test the Market” Usually Creates Problems

Many sellers say the same thing at the beginning of the process:

“Let’s just put it out there and see what happens.”

It sounds harmless.

It sounds flexible.

It sounds low-risk.

In reality, pricing a home “just to test the market” often creates problems that are difficult to undo later.

Buyers don’t see “testing” — they see hesitation

The market doesn’t interpret intent the way sellers do.

Buyers don’t think:

“They’re just testing.”

They think:

“They’re not serious.”

“They’ll probably come down.”

“Let’s wait and see.”

That shift in perception happens immediately — often within days.

Once buyers sense uncertainty, they change how they engage:

fewer showings

softer offers

more aggressive negotiations later

The signal matters as much as the number.

Early positioning shapes the entire listing

The first phase of a listing is not just about exposure — it’s about framing.

Early pricing tells buyers:

how confident the seller is

how competitive the home is meant to be

whether urgency exists

When pricing is vague or aspirational, buyers don’t rush to correct it for you.

They simply move on — or wait.

And waiting buyers rarely pay a premium.

Price reductions don’t reset the conversation

One of the biggest misconceptions is that you can always “adjust later” without consequence.

In reality:

the most motivated buyers see the home first

early hesitation becomes part of the listing’s history

later adjustments feel reactive, not strategic

By the time a price is corrected, the tone has often shifted from interest to leverage.

That doesn’t mean a sale won’t happen —

it means the seller is now negotiating from a weaker position.

Testing creates uncertainty — clarity creates confidence

Buyers respond best to clarity.

Clear pricing communicates:

seriousness

preparedness

awareness of the market

respect for buyer decision-making

Unclear pricing invites:

speculation

caution

delay

And delay is rarely neutral in real estate.

The quiet irony

Sellers who “test” the market are usually trying to avoid risk.

But testing often introduces more risk, not less:

longer time on market

more scrutiny

tougher negotiations

emotional fatigue

A well-positioned price doesn’t guarantee speed —

but it gives you control.

The bottom line

Pricing isn’t about guessing the highest possible number.

It’s about:

sending the right signal

attracting the right buyers

creating momentum instead of hesitation

Homes don’t get their best results by being tested.

They get their best results by being positioned.

And positioning, done intentionally, almost always outperforms trial and error.

What Actually Happens Between Listing and Settlement

Most sellers understand two moments clearly:

the day their home goes live

the day they close

What happens in between often feels vague — and that uncertainty creates unnecessary stress.

So here’s a plain-English look at what actually happens from listing to settlement, without dramatizing it.

Step 1: The listing goes live (and the market reacts quickly)

Once your home is listed:

buyers see it immediately

showing activity (or lack of it) starts fast

early feedback is meaningful

The first 7–14 days usually tell us a lot.

This isn’t about panic or excitement — it’s about information:

Are buyers booking showings?

Are they asking questions?

Are comparable homes getting attention?

This early window helps shape next steps, not final outcomes.

Step 2: Showings, feedback, and adjustment (if needed)

During showings:

buyers are comparing your home to others

price and condition are being weighed together

feedback begins to form patterns

Most adjustments that matter happen early, not months later.

That might mean:

clarifying value

refining presentation

or deciding that no change is needed at all

Nothing here is permanent. Everything is responsive.

Step 3: Offers and negotiation

When an offer comes in, it’s not just about price.

It’s also about:

financing strength

contingencies

timelines

inspection terms

flexibility

A “strong” offer is usually a balance, not a headline number.

This phase is more controlled than people expect — and far less emotional when expectations are clear.

Step 4: Inspections and due diligence

This is where many sellers feel the most tension.

Inspections are normal.

Findings are expected.

Very few homes are perfect — buyers know that.

This stage is about:

distinguishing real issues from minor ones

deciding what’s reasonable to address

keeping the transaction moving forward without overreacting

Deals don’t fall apart because inspections exist.

They fall apart when expectations aren’t managed.

Step 5: Appraisal and financing

Once inspections are resolved:

the lender orders an appraisal

financing moves toward final approval

Most appraisals align with the agreed price when homes are positioned correctly.

If questions arise, there are options:

clarifications

adjustments

or renegotiation

Again — control still exists.

Step 6: Final walkthrough and settlement

Before closing:

buyers confirm the home’s condition

final paperwork is prepared

settlement logistics are handled

By this point, most of the heavy lifting is already done.

Settlement itself is usually straightforward — a formality rather than a surprise.

What most sellers are relieved to learn

The process isn’t chaotic.

It’s structured.

Each step has:

expectations

checkpoints

decisions

options

You’re never guessing blindly.

You’re responding to what’s actually happening.

The bottom line

The space between listing and settlement isn’t a black box.

It’s a sequence of manageable steps — each one giving you more clarity, not less.

When sellers understand the process, they tend to:

worry less

react less emotionally

make better decisions

feel more in control

And control, more than timing or headlines, is what makes the experience smoother.

Why Waiting for the “Perfect Market” Usually Backfires

Many homeowners don’t decide not to sell.

They decide to wait.

Wait for:

better rates

more buyers

less uncertainty

clearer signals

a “perfect” market

On the surface, that sounds reasonable.

In practice, it often creates the opposite result.

The perfect market only exists in hindsight

This is the part that trips people up.

When markets feel clear and obvious, it’s always after the fact.

At the time:

buyers are unsure

sellers are hesitant

headlines are mixed

opinions conflict

There is never a moment where everyone agrees:

“Yes, this is the exact right time.”

Waiting for certainty usually means waiting until the advantage has already passed.

What waiting actually introduces (that people don’t factor in)

Most sellers assume waiting is a neutral decision.

It isn’t.

Waiting introduces new variables:

changes in buyer demand

new competing inventory

shifts in rates or lending rules

personal timeline pressure

life events that don’t wait for markets

Even when prices move favorably, conditions don’t always move with them.

A higher price in a harder market isn’t automatically better.

Why sellers overestimate how “perfect” feels

When sellers imagine a perfect market, they picture:

instant interest

multiple offers

clean negotiations

no stress

That does happen sometimes.

But even in strong markets:

buyers hesitate

inspections still happen

negotiations still occur

emotions still play a role

The difference between a “good” market and a “perfect” one is often much smaller than people expect — but the cost of waiting can be much larger.

Control beats prediction

Here’s the quiet truth most people don’t want to hear:

You can’t control the market.

You can control your strategy.

Price, presentation, positioning, and timing within reason matter more than trying to predict a future version of the market that may never arrive in the way you expect.

Selling isn’t about guessing the peak.

It’s about making clear decisions with the information you have.

Why waiting feels safer than it actually is

Waiting feels safe because it avoids action.

But avoiding action doesn’t remove risk — it just delays it.

Markets don’t pause. Buyers don’t wait forever. Life doesn’t schedule itself around perfect conditions.

Often, the sellers who feel the most regret aren’t the ones who sold and adjusted.

They’re the ones who waited for clarity that never came.

The bottom line

There is no such thing as the perfect market in real time.

There are only:

markets you understand

strategies that fit them

decisions made calmly

Waiting can be the right move — when it’s intentional.

Waiting because you’re hoping for certainty usually isn’t strategy. It’s hesitation dressed up as patience.

And those two feel very different once time passes.

What Happens If My House Doesn’t Sell?

What Happens if My Home Doesn’t Sell? Pennsylvania real estate questions. Homeowners in Bucks and Montgomery County.

This is one of the most common questions sellers have — and almost nobody asks it out loud.

Usually it sits underneath everything else:

What if I price it wrong?

What if the market shifts?

What if I list and nothing happens?

So let’s be clear about something upfront:

A house that doesn’t sell is not a failure.

It’s information.

And information gives you options.

First: most homes don’t “fail” — they stall

When a home doesn’t sell, what’s usually happening is one of three things:

Price and perception don’t line up

The marketing isn’t reaching the right buyers

The strategy doesn’t match the market segment

None of those mean something is “wrong” with your house.

They mean the market is giving feedback.

And feedback is adjustable.

You are never trapped by listing your home

This is the part sellers worry about most — and it’s almost always misunderstood.

Listing your home does not lock you into anything irreversible.

If your home doesn’t sell, you can:

adjust the price

change the marketing approach

pause and reassess

take the home off the market entirely

You are always in control.

There is no penalty for testing the market intelligently.

Why fear makes this question feel bigger than it is

The idea of “what if it doesn’t sell?” often carries a hidden fear:

What if people think something is wrong with it?

In reality, buyers don’t think that way.

Buyers assume:

sellers are testing

sellers are adjusting

sellers are reacting to conditions

A home that doesn’t sell immediately isn’t damaged goods.

It’s a home that hasn’t found its price-positioning balance yet.

That’s normal.

What actually matters if a home stalls

If a home isn’t selling, the important questions are not emotional ones. They’re practical:

Are buyers scheduling showings?

Are they giving feedback?

Are comparable homes moving?

Is the price aligned with buyer expectations today, not last year?

Those answers tell you exactly what to do next.

This isn’t guesswork. It’s pattern recognition.

The quiet truth most sellers never hear

The biggest risk isn’t listing and not selling.

The biggest risk is doing nothing because of a hypothetical outcome that hasn’t happened yet.

Time passes either way. Markets change either way. Life keeps moving either way.

Listing gives you clarity. Waiting often just extends uncertainty.

The bottom line

If your house doesn’t sell, nothing bad automatically happens.

You don’t lose control.

You don’t lose leverage.

You don’t lose options.

You gain information.

And informed decisions are always easier than imagined ones.

Sometimes the most stressful scenario isn’t the one that happens

it’s the one people keep playing in their head.

This is one of those cases.

Do I Really Need a Realtor to Sell My House in Pennsylvania?

Some sellers don’t.

Many think they don’t — until things get complicated.

What Realtors Actually Do

Pricing strategy

Buyer positioning

Negotiation

Inspection management

Keeping deals together

Marketing is only part of it.

When Selling Without an Agent Makes Sense

You’re experienced

You’re comfortable negotiating

You understand local buyer behavior

Bottom Line

The real value isn’t listing — it’s execution.

What Causes Deals to Fall Apart After Inspection?

Most deals don’t fall apart because of defects — they fall apart because of expectations.

Common Deal Killers

Surprises

Poor prep

Weak negotiation strategy

Emotions during inspection

How Sellers Protect Deals

Address obvious issues early

Price realistically

Know where buyers push back

Bottom Line

Inspections don’t have to derail deals — if you plan for them.

Why Do Some Houses Sit on the Market?

Homes sit for predictable reasons.

The Most Common Ones

Overpricing

Poor presentation

Misreading buyer expectations

Ignoring competition

Very rarely is it “just the market.”

Why This Matters

Homes that sit:

Lose leverage

Invite low offers

Require price reductions

Early decisions matter more than later fixes. You don’t want to wind up the home that “has something wrong with it”

Bottom Line

Homes that sell well are positioned well from day one.